Siren Song Capital

Oliver Thompson

February 18th, 2026

Helen of Troy: Ugly, but Still Profitable

Helen of Troy is not a great company. The characteristics that define great businesses and long-term investments are objectively missing here. However, at a certain price, nearly any asset becomes attractive no matter how messy or opaque. I have been seeing this business in my perusing of 52-week low lists, and my initial scan of the Value Line page intrigued me enough to download a decade’s worth of 10-K’s and dig deep. My thesis is this: The only path that justifies today’s valuation is a nonlinear earnings collapse below roughly $50M.

Their shares were bid up well beyond intrinsic value during the coronavirus era and ensuing “everything” bubble in 2021. The market has reassessed the brand durability and earnings power of this business and overshot to the downside well below conservatively estimated intrinsic value. The current price seems to suggest permanent impairment of the company’s brands and ability to generate cash in conjunction with a fear that refinancing debt at maturity becomes costlier. In my opinion, the company’s financial position isn’t as dire as the market is assuming, and even with sustained decreases in revenue, decreasing margins, and higher refinancing costs, Helen of Troy still generates positive owner’s earnings that imply a higher per share intrinsic value than what today’s price suggests.

Business Profile

Helen of Troy operates as a leveraged “serial acquirer” style business that purchases brands they deem cohesive to their overall strategy and business. None of these are incredible brands (notice a theme here?) yet they still command shelf space at big-box retailers and sit squarely in the middle of the pack with many other competitors. Recognizable brands include Hydro Flask, OXO, Osprey, Hot Tools, Curlsmith, Vicks, and Braun. Amazon, Target, and Wal-Mart account for around a third of sales, and the ultra-competitive nature of selling undifferentiated products through these large retailers creates an environment where price becomes one of the main incentives to purchase. Because this is not a long-term franchise investment, I am valuing it as a cash-producing annuity rather than underwriting individual brand moats. My valuation of Helen of Troy is based upon a normalized return to mid-cycle earnings power, conservatively estimated owner’s earnings, and interest costs associated with potentially higher rates come refinancing time.

Financials

The balance sheet and financial metrics aren’t atrocious by any means. As of the latest 10-Q release, Helen of Troy has a current ratio of 2.0, an interest coverage ratio of 2.75 (EBIT/Interest Expense), capital turnover ratio of 2.4, and debt to equity of 1.05. The company is not an equity stub at risk of being wiped out in a restructuring, yet the market is close to pricing it as such. Net margins in 2023-2025 respectively were 7%, 8.5%, and 6.5%. Operating and net margins have not been historically smooth or linear, which is expected given the competitive environment in which they operate. Looking at the 10-year trend, revenues have increased nearly 5% per annum with a peak in 2022 and what I believe is currently a post-covid reversion to the mean given the slight revenue declines over the past 3 years. The most recent fiscal year produced revenues of 1.907B, EBIT of 143M, Net Income of 124M, and owner’s earnings of 200 million (net income plus 55M of D&A, 51M non-cash asset impairment, minus maintenance capital expenditures of roughly 30M). I add back non-cash impairment charges because they reflect prior overpayment rather than current cash cost. Long-term changes in working capital are flat over the decade, and don’t add or subtract from owner’s earnings. Figuring out the sustainability of these cash flows to equity owners and which brands may also be impaired is where the analysis becomes tricky and subjective.

Capital Allocation

This is where the ugliness begins. Several acquisitions, particularly in the beauty segment, appear to have been underwritten too aggressively and have destroyed shareholder value. Continued debt-funded acquisitions at unattractive prices would invalidate or impair (see what I did there?) my thesis. The portfolio of brands as a whole still produces significant revenues and cash flows, but not as much as management or the market originally anticipated. Per the latest filing, the company took asset impairment charges of $800M in the nine months ended November 30th, 2025. This led to a headline earnings figure of -$36.70 YTD which the market reacted sharply to. This looks disastrous, but it doesn’t affect cash flow as it is “only” an accounting item expensed through the income statement, not a death sentence for the business or its brands. They are still generating revenues roughly in line with FY 2025 and producing cash flow for the equity owners. All in all, this is an accounting expense and has more to do with carrying values on the balance sheet as opposed to future cash generation abilities.

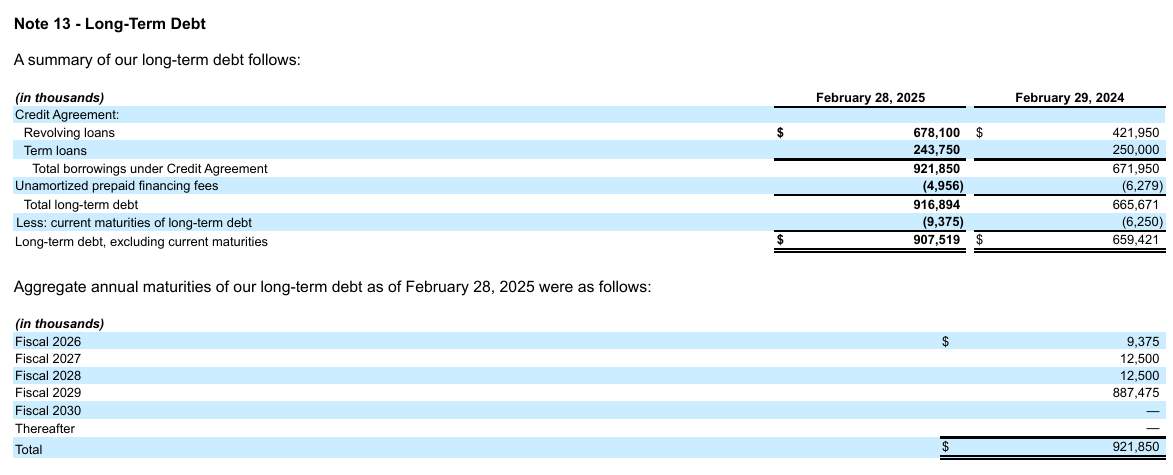

Debt

Since Helen of Troy operates as a roll-up style business that continuously acquires other businesses, debt is a quasi-permanent part of the capital structure. They currently have an equal amount of debt as they do equity due to the recent asset impairments reducing the value of equity. Total debt, as of the latest filing, is 891M with yearly interest charges of 52M. This is currently very manageable as evidenced by the 2.75 interest coverage ratio, but the market is uncertain whether they will be able to refinance at the same rates or incur punitive future rates, further increasing interest expense and reducing cash flows available to owners. Current debt levels and maturities are as follows:

As we can see, there isn’t a real risk to the equity regarding higher interest rates reducing net income until a large amount of debt comes due in 2029. Current weighted average interest rates across all debt carried is 5.6%. The firm is not at risk of breaching any covenants given the temporarily raised leverage ratio following the recent Olive & June acquisition. They are currently allotted a maximum 4.5 leverage ratio which is stepped down gradually to a final maximum ratio of 3.5 after August 31st, 2027. The agreed upon figure used to calculate this is an adjusted EBITDA amount to be used instead of EBIT. As it currently sits, Net Debt/Adjusted EBITDA ratio is 2.7, well below the allowed 4.5 and future stepped down 3.5 ratio.

Valuation

Since this business isn’t a reliable, linear grower, I will use various economic scenarios to come up with a range of values from a slight decline in revenue and margins to a “titanic” level disaster and see how the business holds up in all aspects. I am not attempting to forecast and discount future cash flows but rather use a conservative earnings power valuation and assume the company resembles a perpetuity with permanent loss of earning power. If revenues and margins grow modestly over time, then that will be an unaccounted-for bonus, but this will be a pessimistic valuation where revenues and margins become permanently impaired. Historical net margins over the past decade have been 9% and revenues have climbed 5% per annum when viewed from 2016 to today and ignoring the 2022 peak. I will forecast various revenue declines and net margins to get a range for each scenario and the lower net margins will account for a future increased cost of debt.

For the purposes of brevity each scenario will assume a stated revenue decline, and then test net margins of 9%,7%, and 5%, add back D&A, assume no further impairments to add back which risks overstating owner’s earnings, and finally subtract maintenance capex. I will also apply 10%, 12%, and 15% discount rates to the resulting cash flows and divide by fully diluted shares outstanding. Each row shows estimated owner’s earnings, followed by intrinsic value per share at 10%, 12%, and 15% required returns.

Scenario #1:

Revenue decline of 5%, resulting in a range of owner’s earnings of:

188M = $82 per share, $68, $55

152M = $66, $55, $44

115M = $50, $42, $33

Scenario #2:

Revenue decline of 10%, resulting in a range of owner’s earnings of:

179M = $77, $64, $52

145M = $63, $53, $42

110M = $47, $40, $32

Scenario #3

Revenue decline of 25%, resulting in a range of owner’s earnings of:

153M = $66, $55, $44

125M = $54, $45, $36

97M = $42, $35, $28

Scenario #4

Revenue decline of 50%, resulting in a range of owner’s earnings of:

110M = $48, $40, $32

92M = $40, $33, $27

73M = $32, $27, $22

Note: Even in the lowest scenario, Adjusted EBITDA remains sufficient to keep leverage below the 3.5× covenant threshold.

Conclusion

Helen of Troy is not a high-quality compounder. It is a leveraged portfolio of consumer brands built through acquisition, and management clearly overpaid in prior years. Impairments confirm that earlier growth and margin assumptions were too optimistic. Revenue has declined from pandemic highs and competition has intensified. However, the current stock price reflects more than underperformance. At roughly $17 per share, the market is effectively valuing the company as if sustainable owner’s earnings are $40-$50M or as if the business has a short economic life. That would require revenue to fall materially below $1B and margins to compress well below historical trough levels with no stabilization.

Even under very conservative assumptions such as revenue declining to $1B at 5% margins, intrinsic value remains materially above the current price when capitalized at reasonable required returns. Higher refinancing rates and slower growth do not meaningfully change that conclusion. The only path that justifies today’s valuation is a nonlinear earnings collapse that drives durable equity cash flows below roughly $50 million and keeps them there. That outcome is possible, but it requires a degree of structural decay not yet evident in the historical record. This is not a bet on recovery; it is a bet that earnings stabilize at a reduced but durable level. The disagreement is simple: The market is pricing terminal decay. I believe the probabilities of stabilization are higher.

Disclaimer: I own shares of Helen of Troy, purchased under $17/share. This piece reflects my own research and opinions for informational purposes only. It’s not investment advice, and I’m not recommending anyone buy or sell any security. I may hold a position in the companies mentioned. As always, do your own work and make decisions based on your own analysis.

Leave a comment